A seller credit is money the seller agrees to put toward the buyer's closing costs, written into the purchase agreement and applied at closing. It is sometimes called a seller concession. Instead of cutting the sale price, the seller covers part of what the buyer owes up front, which frees the buyer's cash for the down payment or reserves.

The important limits: a seller credit cannot go toward the buyer's down payment, the buyer cannot receive any of it as cash back, and every loan program caps how much of it a lender will allow. Those caps are the part most people miss until late in the transaction.

This guide covers what a seller credit can and cannot pay for, the actual limits by loan type, why sellers use them, and how to negotiate one from either side.

What a seller credit can pay for

Lenders generally permit a seller credit to cover the buyer's settlement costs and prepaid items:

- Loan costs. Origination, underwriting, processing, and the appraisal

- Title and escrow. Lender's title insurance, escrow fees, recording charges

- Prepaid expenses. The first year of homeowners insurance and prorated property taxes

- Discount points. Buying the interest rate down, either permanently or through a temporary buydown

That last one has become the most strategically useful. A credit spent on discount points lowers the monthly payment for as long as the buyer holds the loan, which for many households does more good than the same money applied to escrow fees.

What it cannot pay for

- The down payment. This is a firm rule across essentially every loan program. Down payment funds must come from the buyer or an allowed gift or assistance program.

- Cash back to the buyer. If the credit exceeds actual costs, the buyer does not pocket the difference.

- Post-closing renovations or personal property. Furniture, appliances not included in the sale, and work the buyer plans to do later fall outside what a lender will approve.

That last point creates a common misunderstanding about repair credits, which is worth its own explanation below.

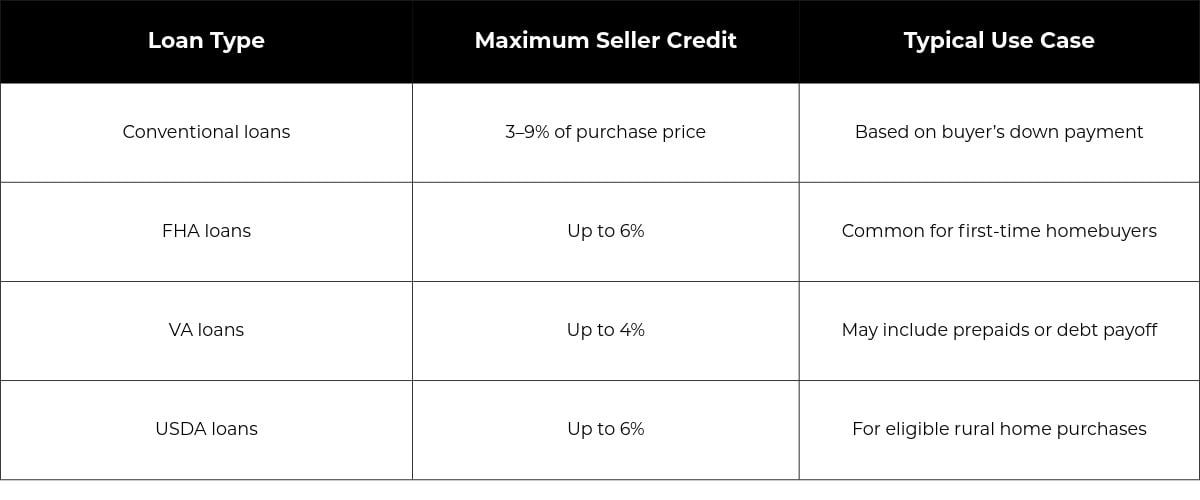

Seller credit limits by loan type

This is where deals actually break, so confirm the number with your lender before writing it into the contract. Limits are set by the loan program and are generally calculated as a percentage of the purchase price.

Two things to know about these. First, the conventional caps move with loan-to-value, which means a buyer putting 5 percent down has far less room than one putting 20 percent down. That is often the opposite of what people assume, since the buyer with less cash is the one who needs the credit most.

Second, these are ceilings, not entitlements. A lender will only allow a credit up to the buyer's actual closing costs regardless of the cap. Program rules also change, so treat the table as a starting point and verify against your specific loan.

What happens if the credit is too large

If the agreed credit exceeds what the buyer actually owes at closing, the excess does not go to the buyer. Depending on the loan, it either gets reduced to match real costs, or it can sometimes be redirected toward a rate buydown or additional prepaid items if the program allows.

The practical outcome is that the seller often keeps the difference, and the buyer got less value than they negotiated for. This is why the credit amount should be set after the buyer has a cost estimate from their lender, not guessed at during the offer.

Appraisal is a separate consideration. A seller credit does not change the appraised value of the home directly. But appraisers do account for concessions when analyzing comparable sales, and if a home sells for $900,000 with a large credit attached, that transaction is not really a $900,000 comp. Unusually large concessions can draw scrutiny.

Why sellers offer credits

To hold the sale price. A $15,000 credit and a $15,000 price reduction cost the seller roughly the same at closing, but the credit preserves the recorded sale price. That matters for neighborhood comparable sales and can matter to the seller's own sense of the deal.

To resolve inspection findings. When a home inspection turns up work the seller does not want to do before closing, a credit lets the buyer handle it themselves on their own timeline.

To widen the buyer pool. In a market with more inventory, a credit toward a rate buydown can bring the monthly payment into reach for buyers who could not otherwise qualify. That is a different lever than price, and sometimes a more effective one.

To keep a deal moving. Late in a transaction, a modest credit is frequently cheaper than losing the buyer and restarting with a home that now has days on market working against it.

Repair credits, and the thing that confuses everyone

When a home inspection reveals problems, sellers often offer what both parties call a repair credit. Structurally, it is almost always processed as a closing cost credit, because lenders will not hand a buyer cash at closing to spend on repairs later.

That distinction has real consequences. If the buyer's total closing costs are $14,000 and the negotiated repair credit is $20,000, $6,000 of it has nowhere to go. The parties then have to restructure, usually as a price reduction instead.

It also means the buyer needs the cash to do the work after closing, which is not always the case for a first-time buyer who just emptied their savings.

Sellers who would rather address issues before listing and avoid the negotiation entirely can look at Every Door Real Estate's Turnkey Services, which covers pre-sale repairs with costs settled at closing. It is one option among several, and plenty of sellers reasonably choose to

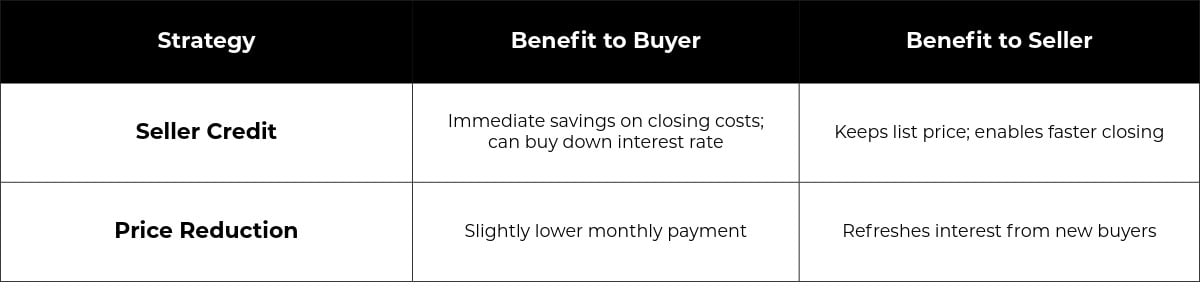

Seller credit vs. price reduction

Which option is better — a seller credit or lowering the sale price? It depends on the buyer’s goals and the current market conditions. Here is a quick comparison:

The buyer's perspective

A seller credit is most valuable to buyers who are cash-constrained rather than income-constrained. If you can afford the monthly payment but are scraping together the down payment plus another $15,000 in closing costs, a credit is the difference between closing and not.

The tradeoff is that if the sale price stays the same, you are financing more of the home's value than you would have with an equivalent price cut. Over a 30-year loan, that costs more in interest than the credit saved you up front. Whether that is the right trade depends entirely on whether you have the cash today.

Practical steps:

- Get pre-approval first, so you know your program's cap

- Ask your lender for a cost estimate before you name a credit amount in the offer

- Consider directing the credit toward a rate buydown rather than fees, if the numbers support it

- Expect to offer closer to list price if you are asking for a meaningful credit

In competitive situations, an offer requesting a large credit reads as weaker than a clean one, even when the seller's net proceeds are identical. That perception is worth accounting for.

The seller's perspective

Run the net proceeds math before deciding between a credit and a price reduction. In most cases they land close together, and the deciding factors are strategic rather than financial:

- A credit holds your sale price for the neighborhood record

- A price reduction is simpler and carries no lender cap risk

- A credit can be targeted, for example specifically at a buydown that solves the buyer's actual problem

- A price reduction reaches buyers browsing by price filter, which a credit does not

The risk to watch is structuring a credit that exceeds the buyer's cap or their actual costs. That gets discovered days before closing, when everyone is least flexible.

Common misconceptions

"A seller credit is free money for the buyer." It comes out of the seller's proceeds and, if the price stays firm, ends up financed in the buyer's loan. It moves money in time rather than creating it.

"You can use it for the down payment." You cannot, on essentially any loan program. This is the most frequent misunderstanding.

"The cap is 6 percent." That is the FHA figure, and it gets repeated as if it applies everywhere. Conventional caps range from 2 to 9 percent depending on the loan-to-value ratio.

"Credits only happen in slow markets." They are more common when inventory builds, but they show up in any market as a tool for resolving inspection findings.

"A credit and a price cut are the same thing." Financially they are close. Strategically, they behave differently for appraisal, comparable sales, and how buyers find your listing.

Where a real estate agent fits in

The failure mode with seller credits is almost always structural rather than adversarial. A credit gets written for more than the loan program allows, or more than the buyer's actual costs, and it surfaces during underwriting when there is no time left to fix it cleanly.

An experienced real estate agent catches that before it goes into the purchase agreement, by asking the buyer's lender what the cap is and what the estimated costs are. On the seller side, they run the net proceeds comparison so the choice between a credit and a price reduction is made with real numbers.

If you are weighing how a credit would affect your bottom line, a free home valuation is a reasonable starting point, and you can contact Every Door Real Estate to walk through the structure for your situation. It also helps to understand the full cost picture on both sides, which our guide to closing costs in Washington State covers in detail.

Key takeaways

- A seller credit covers the buyer's closing costs, prepaid expenses, and discount points. It cannot go toward the down payment, and no cash comes back to the buyer.

- Caps vary by loan program and by loan-to-value. Conventional runs 2 to 9 percent, FHA 6 percent, VA 4 percent for concessions. Confirm with the lender.

- A credit larger than the buyer's actual costs is wasted. Set the amount after the lender's estimate, not before.

- Repair credits are processed as closing cost credits, which limits how large they can be.

- Compare net proceeds before choosing between a credit and a price reduction. They are usually close, and the difference is strategic.

Frequently asked questions

Does a seller credit affect the appraisal? Not directly. The appraiser values the home, not the financing terms. But concessions are factored in when that sale is later used as a comparable, and a large credit can prompt closer review.

Can I use a seller credit for my down payment? No. Down payment funds must come from the buyer's own resources, an approved gift, or a down payment assistance program. This holds across conventional, FHA, VA, and USDA loans.

How much can a seller credit be on an FHA loan? Up to 6 percent of the purchase price, though the credit still cannot exceed the buyer's actual closing costs and prepaid expenses. FHA's relatively generous cap is one reason credits are common for first-time buyers.

Is it better to ask for a credit or a lower price? It depends on your constraint. If you are short on cash at closing, take the credit. If you can cover closing costs and want the lowest long-term payment, the price reduction usually wins.

This article is for educational purposes only and is not legal, tax, or lending advice. Loan program limits are subject to change. Confirm all figures with your lender before writing terms into a purchase agreement.

Check out this article next