In Seattle's fast-paced housing market, how you finance your home purchase can make or break your chances of securing a property. Here's the bottom line:

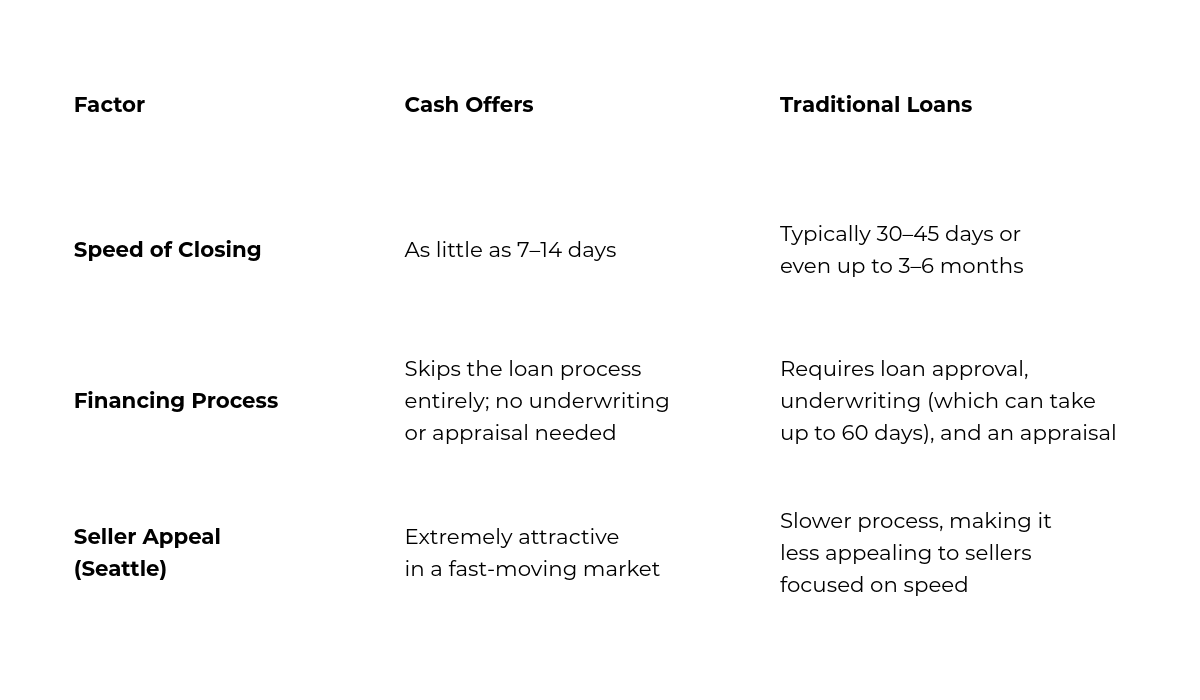

- Cash Offers: Faster closings (7–14 days), no financing contingencies, and highly attractive to sellers. However, they require significant liquid funds and might limit your financial flexibility.

- Loans: Accessible for buyers without large cash reserves, enabling homeownership with smaller upfront costs. But the process is slower (30–45 days) and includes risks like appraisals and financing delays.

Quick Comparison:

Cash offers excel in speed and certainty, while loans provide broader access to homeownership. The best choice depends on your financial situation and priorities.

How Cash Offers Work

Cash offers simplify the home-buying process by eliminating the need for mortgage financing. When buyers have the full purchase price available in cash, they can act quickly and confidently - an advantage in Seattle's fast-paced housing market.

Mechanics of a Cash Offer

At the heart of a cash offer is proof of funds. Buyers need to show they have the full purchase amount readily available before sellers will seriously consider their offer. This proof often comes in the form of recent bank statements, investment account summaries, or letters from financial institutions confirming liquid assets.

Sellers expect this cash to be readily accessible, not tied up in assets like retirement accounts or other funds that are harder to liquidate. Having verified, liquid funds speeds up the process by eliminating the delays that come with mortgage approvals.

Even though cash buyers skip the financing step, they still face closing costs. These may include pre-paid taxes, title insurance, and escrow fees, which vary depending on the property's price and location.

While not mandatory, cash buyers are encouraged to conduct home inspections and appraisals. Inspections can uncover issues such as structural problems or outdated electrical systems, while appraisals ensure the buyer isn't overpaying for the property.

This streamlined process is what makes cash offers particularly effective in the unique conditions of Seattle's housing market.

When Are Cash Offers Common in Seattle?

Seattle's real estate market presents several scenarios where cash offers are especially appealing. In fact, nearly 25% of homes sold in Seattle are purchased with cash, highlighting the influence of the city's high-earning tech professionals and active investors.

Competitive bidding wars are a frequent occurrence in neighborhoods like Fremont or West Seattle. In these situations, cash offers stand out because they are less likely to encounter delays or fall through.

Investor activity also drives a significant number of cash transactions. Real estate investors, often backed by private funding or capital from previous deals, can act quickly on properties - particularly in areas with high rental demand or homes needing renovation.

In sought-after neighborhoods like Capitol Hill, where homes sell quickly, buyers who can close within weeks have a distinct advantage over those relying on traditional financing.

Interestingly, cash offers are 334% more likely to succeed compared to offers with standard financing contingencies. This statistic underscores why many buyers in Seattle strategically use cash to secure their dream home.

Every Door Real Estate notes that Seattle buyers often use cash as a strategic tool, benefiting from the speed and reliability that cash transactions provide.

How Traditional Loans Work

Traditional loans involve buyers securing financing through a mortgage lender, making the process more intricate compared to cash purchases. While it takes longer than a straightforward cash transaction, this method allows buyers without significant cash reserves to participate in the housing market.

Steps in the Loan Process

The journey begins with pre-approval, where lenders assess a buyer's financial health by reviewing documents like pay stubs and tax returns. This step, which typically takes 3 to 10 days, results in a pre-approval letter that strengthens offers in competitive markets like Seattle. However, it’s important to note that pre-approval doesn’t guarantee final loan approval.

Once an offer is accepted, the process moves to underwriting, which can take 30 to 45 days. During this time, underwriters verify financial details and evaluate risks. As part of underwriting, an appraisal is conducted to determine the property’s market value. The final steps - approval and closing - involve signing the necessary documents and transferring the keys to the new owner.

Buyer and Seller Considerations

Traditional financing comes with requirements that cash buyers can bypass. For instance, buyers need a credit score of at least 620 for conventional loans, though FHA loans may accept scores as low as 580. Down payment amounts vary depending on the loan type: conventional loans require anywhere from 3% to 20%, FHA loans require 3.5%, and VA loans allow for zero down. In a city like Seattle, where median home prices exceed $800,000, even a 10% down payment can exceed $80,000.

Additionally, buyers must show a stable employment history and maintain a debt-to-income ratio below 43% to 50%, depending on the loan program.

For sellers, traditional financing introduces some risks and challenges. Financing contingencies give buyers the option to back out if they cannot secure a loan, leaving sellers to start over. Appraisal contingencies can also complicate deals in Seattle's fluctuating market - if the appraised value is lower than the agreed price, sellers may have to lower the price or find buyers willing to cover the gap out of pocket.

Extended closing timelines are another hurdle, increasing the chances of deals falling through. Despite these obstacles, traditional loans remain the most common way for buyers in Seattle to purchase homes, making homeownership accessible even for those without large cash reserves.

Cash Offers vs Traditional Loans: Side-by-Side Comparison

Navigating Seattle's competitive real estate market means understanding the key differences between cash offers and traditional loans. These two approaches can have a big impact on how quickly and smoothly a transaction unfolds.

Comparison Table: Key Factors

Experts point out that avoiding financing contingencies can cut the closing time from over a month to just a couple of weeks. This speed and simplicity make cash offers stand out, especially in Seattle's bustling market.

Seattle Market Trends and Examples

Seattle's real estate market mirrors national trends, with cash offers hitting a 10-year high in February 2024. They accounted for 32% of all home sales during that time. This surge highlights how cash offers have become an increasingly popular strategy.

For buyers relying on traditional loans, the process can be lengthy. Even preapproved buyers still need to complete the final steps of mortgage underwriting:

In February 2024, 33% of buyers, including real estate investors, opted to pay in cash. This growing trend reflects how cash offers give buyers a competitive edge, especially in multiple-offer situations. Without the uncertainty of mortgage underwriting - which can take up to 60 days without a guaranteed outcome - cash buyers are seen as a safer bet for sellers.

For sellers, the benefits go beyond speed. Kris Lindahl explains:

"A guaranteed cash offer drastically reduces the time it takes to sell a home. With no need for bank approvals, appraisals, or extended negotiations, it's one of the fastest ways to sell your property."

This combination of speed, simplicity, and reduced risk makes cash offers a powerful option in Seattle's fast-paced housing market.

Pros and Cons for Buyers and Sellers

Making the right choice in Seattle's competitive housing market means understanding the upsides and downsides of each approach, whether you're buying or selling.

Pros and Cons for Buyers

Cash offers come with some serious perks for buyers. They provide strong negotiating power, which can be a big deal when competing against multiple offers. Sellers often lean toward cash offers, even if they're slightly lower, because they bring speed and certainty. Without the need for loan approvals, appraisals, or underwriting, cash deals can wrap up much faster.

Another advantage? Cash buyers have more flexibility in negotiations. They can skip inspections or buy a home "as-is", which isn't always an option for those relying on financing. This flexibility can be a game-changer in a market where homes are snatched up quickly.

But there’s a catch: cash offers require a lot of liquid capital. Plus, you lose out on the benefits of financial leverage. For example, with a traditional mortgage, you could buy an $800,000 home with just a 20% down payment, keeping the rest of your cash for other needs.

Traditional loans, on the other hand, open up opportunities for buyers who don’t have access to large sums of cash. Financing allows many people to buy homes they couldn't afford outright. Loans also help with cash flow management, leaving funds available for things like home upgrades, moving costs, or unexpected expenses. Another potential advantage? Mortgage interest might be tax-deductible, which isn't the case with cash purchases.

However, financing comes with its own challenges. The process takes longer and carries some uncertainty. Underwriting, appraisals, and financing contingencies can slow things down or even make sellers hesitant to accept your offer.

Pros and Cons for Sellers

For sellers, the decision often boils down to their priorities: speed and certainty versus a potentially higher sale price.

Cash offers are appealing because they eliminate many of the delays that come with financing. Without appraisals, underwriting, or lender requirements, cash deals usually close quickly and with fewer hiccups.

That said, cash buyers sometimes offer lower prices. They may bid below market value, prioritizing a fast and hassle-free process over paying a premium.

Traditional loans, by contrast, often result in higher sale prices. Since most buyers rely on financing, it opens the door to a larger pool of potential buyers and more competitive offers. However, the process can take longer, and there’s always the risk of complications - like a low appraisal or loan approval falling through - that could delay or even derail the sale.

Ultimately, sellers need to decide what matters most: a quick, certain sale or the potential for a higher price and broader buyer interest.

Choosing the Best Option for Your Seattle Transaction

Deciding between a cash offer and a traditional loan isn’t straightforward - it all depends on your financial situation, timeline, and priorities in Seattle’s ever-changing market.

For buyers, cash offers can give you a significant edge. If you have the funds available, these offers can speed up the process, eliminate financing delays, and often outshine competing bids. But there’s a catch: using cash might drain your savings and limit your ability to invest elsewhere. In many cases, traditional financing is a smarter choice, allowing you to keep more cash on hand for other opportunities. It’s all about balancing short-term gains with long-term financial health.

For sellers, the decision revolves around your goals. If speed and certainty are at the top of your list, cash offers can be a great fit - even if they come in slightly lower than financed offers. On the other hand, if your priority is to maximize your sale price, traditional financing opens the door to a larger pool of buyers, often leading to higher offers.

Market timing is another factor to consider. In Seattle’s busy spring and summer months, when competition heats up, cash offers tend to carry more weight. But during slower seasons, financed offers become more common, giving buyers more breathing room to navigate the loan process.

Key Takeaways

Your financing choice impacts three main areas: speed, negotiating power, and overall costs. Cash offers are unbeatable when it comes to speed and negotiation leverage, but they require a significant upfront investment. Traditional loans, while more flexible and easier on your cash reserves, require more time and add layers of complexity to the transaction.

Every Door Real Estate’s team of experts can help you navigate these choices with insights tailored to Seattle’s market. Their local specialists provide custom property valuations and strategic advice to match your unique needs. Whether you’re weighing the pros and cons of a cash offer or exploring financing options, they’re here to help you make informed decisions and achieve successful outcomes.

FAQs

What are the benefits of making a cash offer in Seattle’s housing market?

In Seattle’s fast-moving housing market, making a cash offer can set you apart from other buyers. Sellers often prefer cash offers because they remove the risk of financing falling through and can help close the deal faster. This added certainty can make your offer much more attractive.

Going the cash route also gives you more leverage during negotiations. Sellers are often drawn to the simplicity and speed of a cash deal, which can work in your favor. Plus, skipping the mortgage process means you’ll avoid certain fees and costs tied to loan approvals, potentially saving you money. In a market as competitive as Seattle, these perks could be the key to landing your ideal home.

Why do financing contingencies make traditional loan offers less appealing to sellers?

Financing contingencies can be a sticking point for sellers since they hinge on the buyer successfully obtaining a loan. If the loan gets delayed or denied, it can slow down the closing process - or worse, derail the entire deal. In fast-paced markets like Seattle, sellers often lean toward cash offers because they tend to close quicker and come with fewer potential hurdles.

For buyers relying on traditional loans, making your offer stand out is key. You can do this by offering a higher price or showing flexibility with terms, which can help make your bid more appealing in a competitive environment.

What should buyers think about when choosing between a cash offer and a traditional loan for a home purchase?

When choosing between a cash offer and a traditional loan, it’s important to weigh your financial flexibility and long-term plans. A cash offer can streamline the buying process, make closing simpler, and give you a stronger edge in negotiations - especially in competitive markets like Seattle. But keep in mind, it requires a substantial amount of cash upfront, which might limit your ability to invest elsewhere or cover unexpected expenses.

A traditional loan, on the other hand, spreads out the cost over time and may come with potential tax perks. However, it also means dealing with interest payments and a lengthier approval process. To make the right choice, think about the current market, your financial goals, and how quickly you’re looking to close the deal.

Check out this article next