Most people treat title insurance like a toll booth on the way to closing. You pay the number on the screen and keep driving. But in Washington State, that number is actually three or four different charges bundled together, and only one of them is the regulated insurance premium. The rest? Fees, service charges, and add-ons that vary more than most buyers and sellers realize.

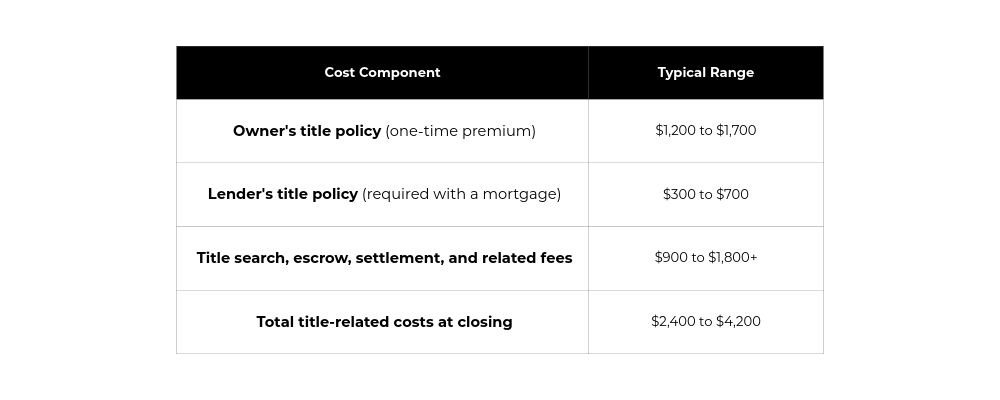

Here's what a typical title-related bill looks like on a $500k to $650k home purchase in Western Washington:

That spread between $2,400 and $4,200 isn't random. It's driven by which title company you use, which discounts you qualify for, how the transaction is structured, and whether anyone bothered to ask the right questions before closing day.

This guide breaks down every piece of that bill, shows you where the real leverage is, and gives you a checklist to catch errors before they become expensive.

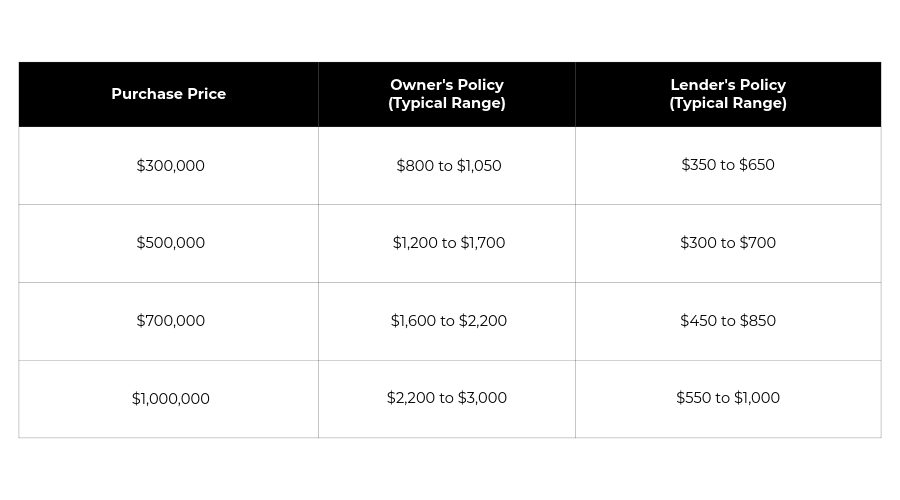

How much does title insurance cost in Washington by home price?

Before we get into the mechanics, here are the numbers most people came here for. These ranges reflect typical owner's and lender's policy premiums in the King/Pierce/Snohomish pricing bands, based on filed rate schedules from major underwriters.

Exact premiums depend on the title insurer and underwriter, the policy type (standard ALTA policy vs. extended homeowner coverage), the rate region, and whether you qualify for a simultaneous issue discount or a reissue rate. Use these as planning numbers, not promises. For a personalized estimate, contact a local title company office directly.

One pattern worth noting: title insurance premiums scale with property value, but not proportionally. The effective rate per $1,000 of coverage declines at higher price points.

What that means in practice:

- Title insurance is a bigger percentage cost on starter homes

- It becomes a smaller percentage cost as prices rise, even though the dollar premium increases

A buyer spending $300,000 pays more per dollar of coverage than a buyer spending $1,000,000. The premium doesn't double just because the home price doubles.

What you're paying for with Title Insurance

Most buyers say "title insurance" when they mean a bundle of separate charges. On your Loan Estimate and Closing Disclosure, you'll see items grouped under several categories. Understanding what falls where helps you spot errors and ask better questions.

These premiums typically appear under "Title: Owner's Policy" and "Title: Lender's Policy" on your Closing Disclosure.

The transaction part

These are the operational costs of getting from signed purchase agreement to recorded deed:

- Title search and title examination (reviewing the chain of title, public record, and recorded encumbrances for errors or defects)

- Escrow and settlement fee (handling funds, instructions, payoffs, recording logistics)

- Document prep, courier, wire, eRecording, and notary fees (varies widely by company)

- Recording fees (mostly pass-through government charges, less shoppable)

- Endorsements (optional add-ons to the base ALTA policy that extend coverage for specific risks)

This is where two closings on the same purchase price can produce very different totals. The insurance premiums might be nearly identical. The fee packages won't be.

What is Washington's filed-rate system?

Washington uses a filed-rate system. Title insurers file rate schedules with the state, and those rates must meet regulatory requirements. In practice, this means:

- Premium differences between major underwriters tend to be modest

- Fee schedules and settlement charges can vary significantly more

- The shopping opportunity is usually in fees and structure, not a dramatic premium discount

When someone tells you "title insurance is basically the same everywhere," they're looking at one line item on the Closing Disclosure and ignoring three others. For additional information on Washington's regulatory framework, visit the Office of the Insurance Commissioner.

The two discounts that save you real money

Simultaneous issue

If you buy an owner's policy and a lender's policy at the same closing from the same company, the lender's policy is typically priced at a reduced simultaneous issue rate. This applies whether you're buying a $350,000 condo or a $1.2 million single-family home.

The combined discount can reduce your total premium by several hundred dollars. It's standard practice, but you should still verify it appears correctly on the draft Closing Disclosure before you sign anything.

One Washington-specific quirk: in some rate regions, the lender's simultaneous issue charge can look close to flat at certain price tiers. Don't assume the math is right. Ask your escrow or title company to show how the lender premium was calculated under the applicable schedule.

Reissue rate

A reissue rate is a reduced premium available when the property was previously insured within a certain timeframe, often within the last several years, though requirements vary by underwriter. It also commonly applies in a refinance scenario, where you're replacing an existing loan rather than purchasing.

To qualify, you'll typically need to provide documentation: a copy of the prior owner's policy or a form confirming the previous coverage. If the prior policy is lost, some title companies can locate the information through their own records.

This is important: The reissue rate isn't automatically applied in every transaction. If you don't ask, or don't provide the source documents, you may pay the full premium unnecessarily. This is one of the most commonly missed savings in Washington real estate closings.

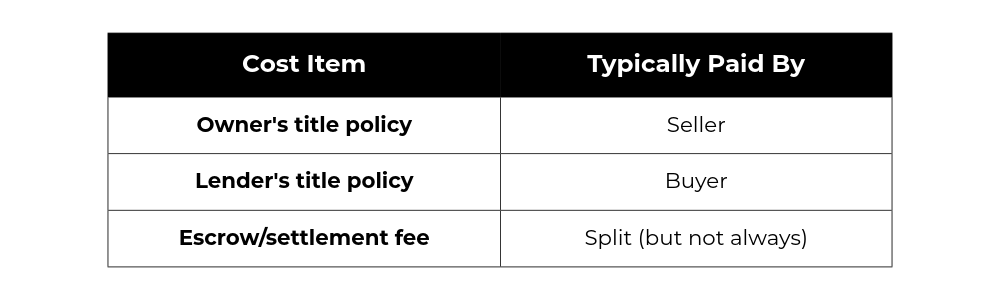

Who pays for title insurance in Washington State

Washington generally follows local custom, not a hard legal rule. The purchase and sale agreement controls.

Common payment pattern in many Western Washington transactions:

But market conditions shift behavior. In a seller-favored market, buyers may agree to take on more of these costs. In a buyer-favored market, sellers may cover more as a concession. For a complete breakdown of typical seller costs in Washington, including title fees and other obligations, see our detailed guide.

If you're selling quickly in a competitive market, understanding which costs you can negotiate helps you close faster and with fewer surprises. The place to negotiate who pays is the purchase and sale agreement, and your real estate agent should be advising you on what's standard in your local market.

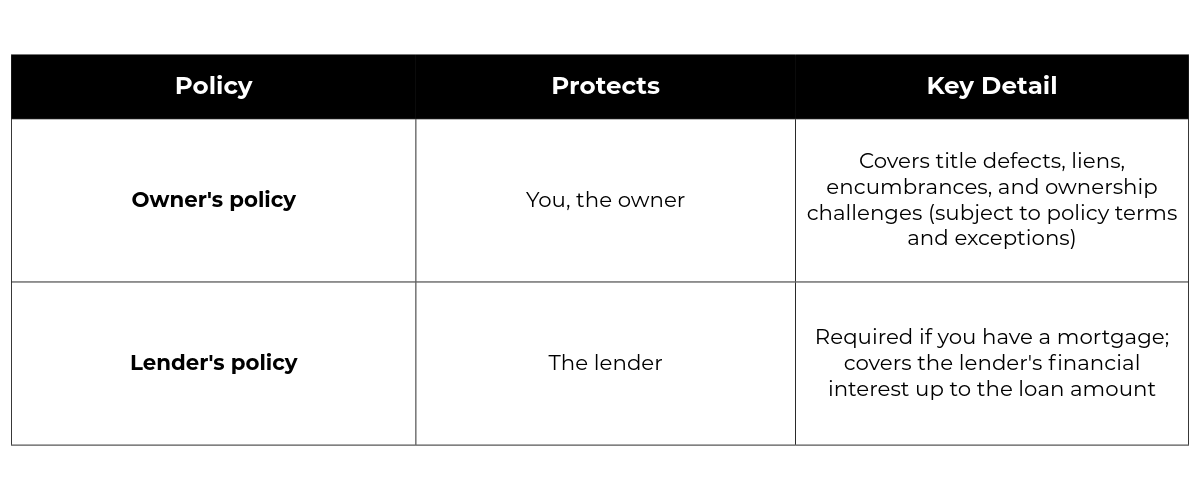

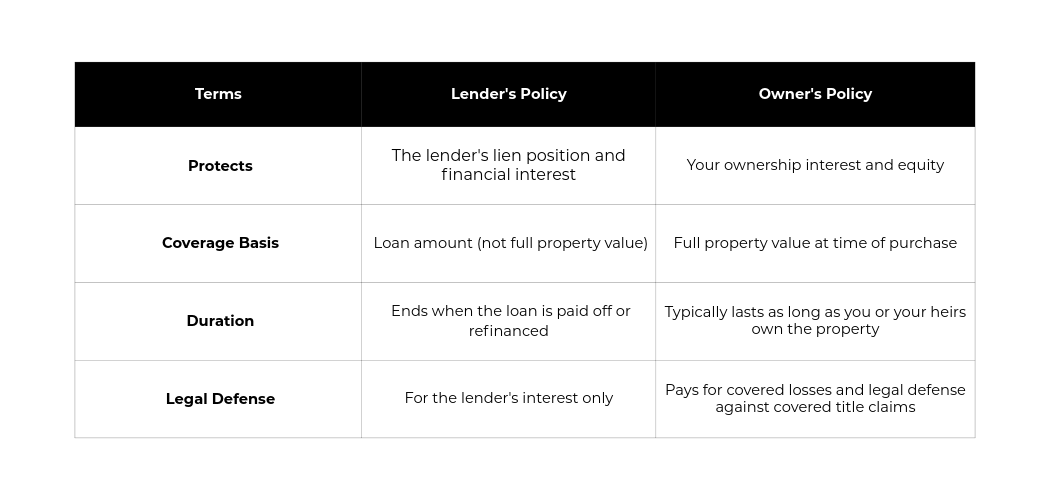

Owner's vs. lender's policy: the distinction that matters

The lender's policy is required paperwork if you're borrowing. The real decision point is the owner's policy, and skipping it is almost always a false economy.

If a title issue surfaces years after closing, the lender's policy is designed to make the lender whole. That does not automatically make you whole. An owner's policy protects you against financial loss from hidden defects, forgery, or undisclosed liens that survived the title search. For most homeowners, paying a one-time premium at closing is far cheaper than hiring a real estate attorney to defend your ownership rights later.

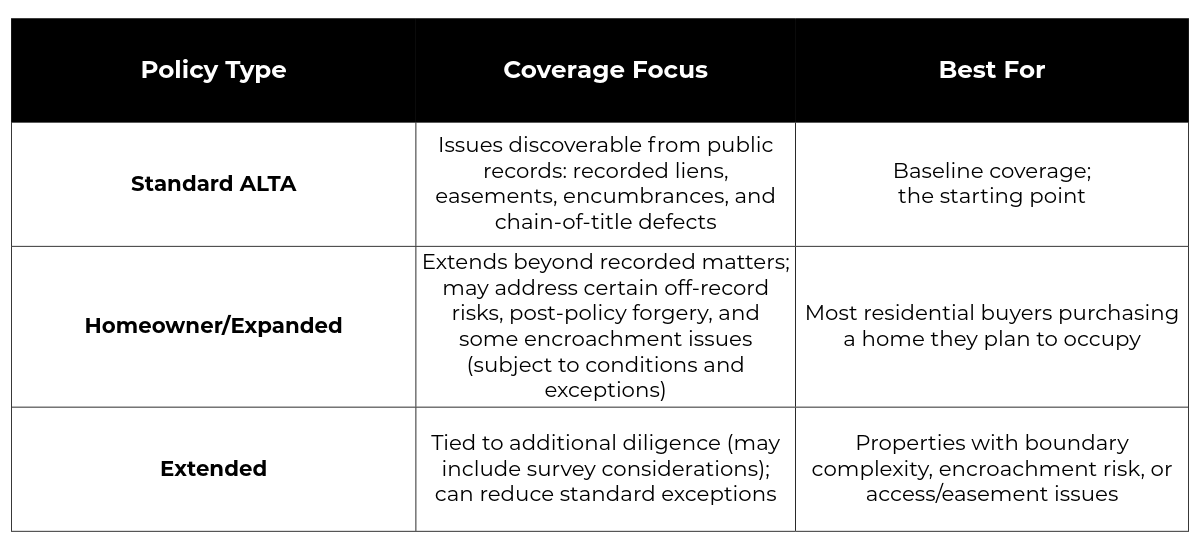

Policy types: standard, expanded, and extended coverage

Washington buyers typically encounter several forms of ALTA policy. The names vary by underwriter, but the practical differences usually look like this:

For most everyday suburban purchases, expanded or homeowner coverage is the sensible middle ground. It's the most popular choice for residential buyers in Washington, and the additional cost over a standard policy is usually modest.

Consider extended coverage when:

- Boundaries are complicated or unclear

- Improvements sit close to lot lines (possible encroachments)

- Rural acreage has access or easement complexity

- You have specific concerns from inspection or record review

Extended coverage isn't automatically better. It's better when your property facts justify it.

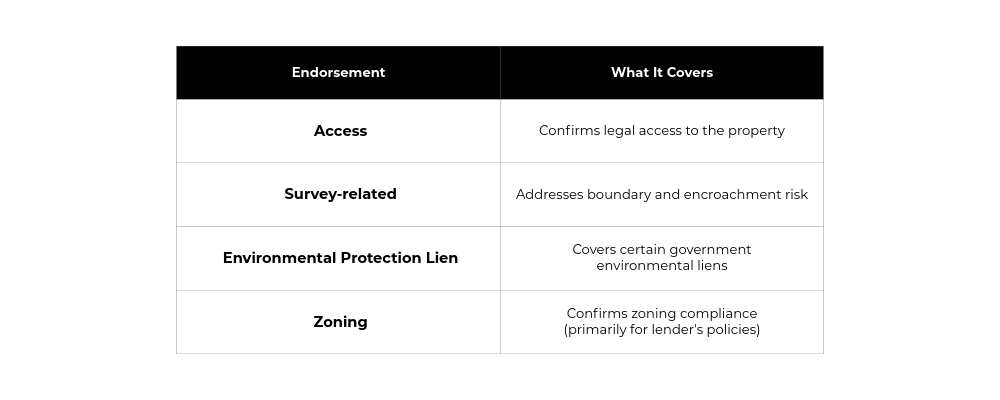

Endorsements: add-ons that fill specific coverage gaps

Endorsements are supplemental attachments to a base ALTA policy that expand or modify coverage for specific risks. Think of them as riders on a standard insurance policy. Common endorsements in Washington include:

Each endorsement adds a fee, typically $25 to $200+. Not every endorsement applies to every transaction type, and availability varies based on underwriter requirements and the property's title search results.

Whether you should add endorsements depends on your property and risk tolerance. Your title company or real estate attorney can help you evaluate which ones apply. The key is that endorsements show up as individual line items on your Closing Disclosure, so you can see exactly what you're paying for and make an informed decision.

5 ways to lower your title insurance cost in Washington

1. Confirm the simultaneous issue structure

If both policies are being issued, ensure the lender's policy is priced at the simultaneous issue rate. Don't assume. Verify on the draft Closing Disclosure.

2. Ask about the reissue rate

If the property was insured relatively recently, or if you're refinancing, you may qualify for a reduced premium under the insurer's filed rules. These discounts often require documentation. If you don't ask, you may not get it.

3. Shop the fees, not just the premium

Request a written, itemized estimate that separates:

- Owner's premium

- Lender's premium

- Escrow and settlement fee

- Title search and exam charges

- Endorsements

- Document, wire, courier, and notary add-ons

Premiums may be close based on filed rates. Fees and endorsements are where the spreads show up.

4. Negotiate a credit instead of arguing line items

If you want relief on cash-to-close, the cleanest method is often a seller credit rather than haggling over individual line items. You end up with the same outcome (less money out of pocket) with fewer complications. Both parties to the transaction benefit from a simpler closing.

5. Surface complexity early

Some costs rise with transaction complexity: multiple parcels, prior boundary adjustments, estate or probate conveyances, unresolved liens, tax obligations, or unusual entity ownership. You can't always control the complexity, but you can control how early you surface it. The earlier the escrow and title office knows what they're dealing with, the fewer rush fees and last-minute fixes you'll face.

How to be aware of wire fraud

Wire fraud is one of the fastest-growing threats in real estate transactions, and it intersects directly with the closing and settlement process.

Here's the typical scheme: a criminal intercepts email communications between the buyer, agent, or escrow office and sends fraudulent wiring instructions. The buyer sends their closing funds to the wrong account, and the money vanishes. The payment is nearly impossible to recover once it's made.

How to protect yourself:

- Always verify wiring instructions by calling your escrow or title company at a phone number you've independently confirmed. Never use contact information from an email.

- Be suspicious of any last-minute changes to wire instructions.

- Ask your title company what anti-fraud protocols they have in place.

Some title companies now offer wire fraud protection services or partner with secure transfer platforms. For more guidance on protecting yourself from real estate fraud, including wire fraud and other common scams, see our detailed guide.

How title costs fit into your total closing costs

Title premiums and related fees are meaningful, but they're rarely the biggest check you write when buying a home.

Buyer closing costs commonly land around 2% to 5% of the purchase price depending on loan structure, points, credits, prepaid items, and timing. Title, escrow, and related services are a mid-sized slice of that total, usually smaller than prepaid tax and insurance or lender origination fees. To learn more about what makes up these costs, see our guide on total closing costs in Washington.

The practical takeaway: optimize your title and escrow costs, but don't lose sight of the bigger levers. Your interest rate, loan origination fees, credits, and prorations will almost always have a larger impact on your total cash-to-close.

Your closing disclosure checklist

Before closing, ask for the draft Closing Disclosure and confirm every line:

- Owner's and lender's policies are correctly listed and not duplicated

- The lender's policy reflects simultaneous issue pricing when applicable

- Any eligible reissue rate discount is applied and documented

- Endorsements are itemized and you understand what each one covers

- Escrow and settlement fee matches the amount you were quoted

- Wire, courier, and document fees look reasonable and aren't stacked

- Recording fees are clearly identified as pass-through government charges

- The deed and transfer documents are in the correct form

Review each line item carefully. Errors on the Closing Disclosure happen more often than you'd expect. This is the moment when "it's only a few hundred dollars" is either true or expensive.

If you're working with Every Door Real Estate, your agent can walk through the Closing Disclosure with you and flag anything that looks off before you get to the signing table.

Key takeaways of title insurance in Washington State

In Washington State, title insurance premiums are regulated enough that the base numbers don't swing wildly between companies. But your total title-and-escrow spend can vary by more than a thousand dollars based on discounts applied, fee schedules used, endorsements added, and how the parties to the transaction agreed to split costs.

Plan on a one-time premium for the owner's policy (typically paid as part of closing), treat the lender's policy as required if you're financing, and put most of your shopping energy into fees, endorsements, and the two key discounts: simultaneous issue and reissue rate.

The buyers and sellers who spend the least on title aren't the ones who found a secret loophole. They're the ones who read the Closing Disclosure line by line, asked their title company to explain what they didn't recognize, and verified every discount before signing. That's a thirty-minute investment that routinely saves hundreds of dollars.

Check out this article next